A credit score is a number that denotes the creditworthiness of any person based on several financial factors. These factors determine their spending lifestyle and the frequency of on-time payments. A credit score is a number that is always represented in three digits that levies great importance for lenders. Lenders consider the credit score written on the credit report to grant or reject a credit application. The credit application can be for loans, mortgages, or even a credit line like credit cards.

The credit score is segregated into two main branches: good credit score and bad credit score. A good credit score will result in favorable terms and conditions, and the credit application will be approved. In contrast, a bad credit score means bad news for the borrower. The reason is that the credit application will receive a refusal. If any creditor agrees to approve the application, a high-interest rate and unfavorable terms and conditions will be put in place.

Credit scores show lenders and creditors a clear picture of the borrower regarding the risk they pose. If the credit score is low, then the risk will be greater. Alternatively, the higher the credit score, the lower is the risk. Credit score and risk are inversely proportional to one another. So if one increases, the other will decrease. Similarly, if one decreases, the other will increase. The risk indicates the ability of the borrower to pay their dues on time.

The credit score of each individual might differ from another borrower depending upon their financial situation. The lenders assess the credit application by looking at the credit report of each individual and making the decision about the credit limits, loan terms, and interest rates.

Credit scores are calculated by taking out information from your credit accounts. The credit bureaus have all the necessary information available to do. These credit bureaus are not affiliated with any bank or credit union as they are separate entities and are also accredited institutions. These bureaus make up the credit report, and creditors and lenders rely on this report before making a final decision.

Different credit scoring systems have one purpose: to calculate individuals’ credit scores to determine their creditworthiness. Each credit scoring system calculates the credit scores in a unique way that is different from one another.

The article will look at the importance of credit scores and then discuss the different factors that directly impact credit scores. We will highlight the various credit scoring systems and briefly discuss how credit scores are calculated. We will look at the scenarios that can result in a good credit score and cause a poor credit score. We will also discuss the different ways to achieve free credit scores. A FAQs section will be included to answer the general queries about credit scores.

Let us look at the reasons that make credit scores vital.

The Purpose of a Credit Score

The credit score is crucial for companies that operate as lenders or credit card issuers for people to ease their financial burden. To do their work effectively, they need a third party to carry out their due diligence on the individual’s financial history to know more about them. In this way, these companies can assess the risk they are taking by approving a loan or credit to such people.

Lenders would like to know that their investment by giving funds to such individuals will be returned with interest as their profit. Many credit card companies offer top-tier credit cards to those with a high credit score. These top-tier cards will consist of those cards that offer more fabulous perks like rewards credit cards, travel credit cards, etc. As a result, individuals need to meet the minimum criteria to qualify for such cards. And the first thing credit card companies look at when they receive a credit application is the person’s credit score.

Many credit card companies have segregated their products and services according to their credit scores. So if your credit score falls in the ‘average’ score range, you will not be able to qualify for cards that are up and beyond this range. Some credit card companies advertise their credit cards based on the credit score, interest rate, and APRs that fall under the score range.

Several companies that provide loans and mortgages operate similarly to credit card companies. The credit score is an essential element by traditional banks, lenders, and credit unions regarding whether you are suitable for the loan. If a person has a lower than average credit score, the loan amount might be approved with strict limitations, including frequent repayment periods and higher repayment amounts. The interest rate charged on such loans will also be relatively higher.

The credit score is vital because it affects whether a person will get approval for the final products or services. Moreover, it will show a person’s terms and conditions to comply with if they get approval, like interest rate, loan periods, APRs, etc.

Let us look at the factors that make up the credit score.

What Items Affect the Credit Score?

In the previous section, we discussed the purpose of the credit score and highlighted its importance for companies and individuals. Here, we shall look at the factors that make up the credit score and discuss their significance.

The credit score is divided into five segments, and each segment has its weightage that affects the credit score. The following factors impact the credit score:

Payment History

Payment history accounts for 35% of an individual’s overall credit score, so it should be catered to with immediate priority. Payment history consists of all past payment records and includes the due dates and when the transactions were paid to the creditor. It is evident that paying the due promptly and within the due date will positively impact the credit score.

Bills include credit card bills, loans, mortgages, and other lines of credit, which should be paid on time. If a person does not pay dues on time, it will hurt their credit score. Unpaid dues can go to a debt collection agency which will become part of the credit report for up to seven years, thus resulting in low credit scores.

Under this category, apart from late payments, several other payment-related information can cause severe damage to the credit score. They include bankruptcies, charge-offs, foreclosures, etc., directly related to low credit scores.

It can take a small amount of time to inflict damage to the credit score negatively, but it can take time and effort to increase it.

Credit Usage

The second factor after payment history that is of immediate importance is credit usage, as it accounts for 30% of a person’s credit score. As the name suggests, the credit bureaus evaluate how much of the debt you owe to creditors under this category. The bureaus consider the debt owed relative to the overall credit limit a person can use.

Under this category, it is crucial to discuss the credit utilization ratio: the low balance to limit ratio and the lower the rate, the better. A low credit utilization rate makes it easy to keep a stable credit score that would improve the points that impact the creditworthiness of a person. It is one of the leading factors that can positively or negatively affect the credit score. It all depends on how a person is keeping their finances.

Financial experts say to keep this rate below 30% and consider that all credit amount needs to be returned with interest within the due date.

A large proportion of credit usage weightage goes into large installments, such as mortgage payments, car loans, student loans, or credit card payments. So it is wise to clear off such debts before the due date. One mistake that people often make is that they delay the payments to the due date, and when the date arrives, they are not financially strong to pay back all the dues. As a result, late payments affect the credit score adversely.

Length of Credit History

Another factor that directly impacts the credit score is the length of credit history which accounts for 15% of the overall credit score of a person. The weightage is relative to a more significant proportion and should be treated with care. This category considers the account’s age under the borrower’s name and the average age of credit accounts, including old and new accounts.

Under this category, the time of the account is vital for the credit score. Old accounts are treated like royalty in this category, so if your account were opened a long time ago, it would positively impact your credit score.

Many people, who have recently opened an account and require urgent funds, can apply for a loan with the help of an authorized user. The authorized user can be a friend or family member who has an older account that is well maintained can help strengthen the average age of the credit. As a result, the credit score will also be boosted.

New Credit

New credit is another factor that affects the credit score as it accounts for an absolute 10% of a person’s credit score. As the name suggests, the credit bureaus consider the new credit a person borrows or has applied for, which is shown in the creditors’ inquiry on the credit report. When a person applies for new credit, lenders will carry out a soft inquiry while other lenders can make a hard inquiry.

A soft inquiry is a personal inquiry that will be done at the lenders’ end and is not reported to the credit bureaus and so will not appear nor affect the credit score in any way. With a hard inquiry, the information is noted in the credit report, and it negatively impacts the chances to improve the credit score. Some lenders do carry out a hard inquiry. And thus, if you have applied for a new credit card loan, it will negatively affect your credit score by decreasing it.

Under the new credit category, credit bureaus will also see how many and when the new accounts have been opened, which will surely decrease the credit score. Credit bureaus believe that opening new credit accounts means that the person is having financial trouble. It is unlikely that they will pay their dues on time, and to avoid that, they are opening new accounts to pay the dues. This is also given the name of “credit risk.”

Credit Mix

The last factor that impacts the credit score is called credit mix, which considers the different types of accounts that show in an individual’s credit report. Due to the nature of this category which accounts for 10% of the overall credit score, people should consider the different credit they are utilizing. Moreover, they should know that all their credit is a “loan” that needs to be returned with interest.

Some common accounts that can show up on the credit report would include the following:

- Credit cards

- Loans (car loans, installment loans, etc.)

- Mortgage (house or other properties)

- Retail accounts

- Finance company accounts

Financial experts argue that it is beneficial to have different accounts, but paying the dues on all such accounts is crucial. Doing so will boost the credit score. Some people apply for short-term loans that may appear in this category. Such a loan has a repayment period of less than one year, and paying back the loan will positively impact your credit score.

Having different accounts is one thing and paying them back in due time is another thing. If people continue to return the payment with interest, keeping in view the terms and conditions of the credit, they are safe and on route to boosting their credit score. If that is not the case, then any unpaid dues will have negative consequences, which will show on their credit report.

Let us look into the different credit scoring systems that all the lenders widely accept.

Credit Scoring Models

All the creditors, banks, and credit unions accept two credit scoring models in the industry. The financial bureaus use these models to conclude the credit score of any person. Let us discuss these models one at a time.

FICO Scoring Model

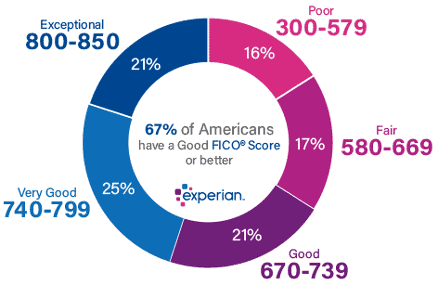

All the lenders use the FICO scoring model to check a person’s credit score. The model has a score range from a minimum of 300 to a maximum of 850. The model depicts a person’s likelihood to return the amount borrowed from the lender. It denotes the risk a lender is taking by approving the credit for that person.

The lower the risk, the higher is the probability that the investment will be returned with interest. Alternatively, the greater the risk, the lower the chances that the investment will be returned on time as default payments may occur. The FICO scoring model has different score ranges and descriptions for each range.

The picture shows the banking industry in the USA and how the people’s credit scores were divided based on their creditworthiness. For instance, 21% of Americans had Exceptional credit scores, while 21% of Americans also had good credit scores. In contrast, the higher proportion of credit scores was labeled “very good”, with 25% of people’s credit scores falling.

As per the image, a score of 700 is considered good, and people can receive favorable interest rates along with terms and conditions for the line of credit. Some people have a credit score of 800 and beyond, which means these people can qualify for top-tier credit cards like travel and rewards cards with low interest. Most people fall in the range of 600 to 750, and the average score lies between these ranges.

Even though high credit scores will boost the confidence of the creditors that you are suitable for the credit or loan, there is still some risk at the lender’s end. Even if a person has an excellent credit score, the risk at the lender’s end remains and will not be eliminated.

Creditors have ranges that they consider good, bad, and average. So people should always go with a positive mind when applying for a loan because creditors’ ranges are sometimes different from the scoring models. So if you think you are a little short on the credit score for being “good”, as per the creditors, you might still be.

Vantage Scoring Model

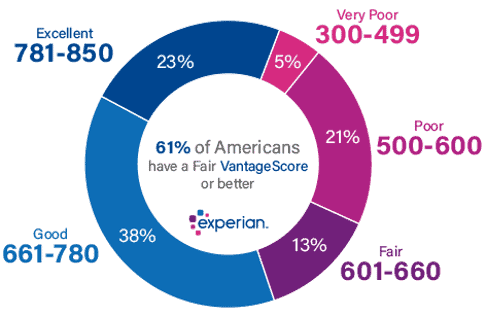

After the FICO scoring model, the next most popular credit scoring model is called the Vantage credit scoring model. This model has a credit scoring range similar to the FICO scoring model, with 300 being the minimum credit score and 850 being the maximum credit score.

The model has the same credit scoring rules as the FICO scoring model: the lower the credit score, the higher the risk for creditors. Moreover, the higher the credit score, the lower the loan application’s chances of rejection. Lenders evaluate their risk assessment by catering to the risk that appears by checking the people’s credit score who apply for a line of credit application.

The Vantage scoring model has different score ranges and descriptions for each range.

The picture shows how the American financial industry divided people’s credit scores into different categories. For instance, 23% were given an “excellent” credit score, while most people fell in the “good” credit score category, accounting for 38%. This shows that most people had good credit scores, between 661 to 780.

How to Calculate the Credit Scores?

Three major credit bureaus calculate the credit scores. These agencies are responsible for gathering data from credit card companies, banks, credit unions, creditors, lenders, and other financial institutions to better evaluate a person’s financial standing. An individual’s credit report is created through the data accumulated by the credit bureaus for credit.

Credit bureaus use the FICO and Vantage scoring model to interpret the credit report results. Each factor that affects the credit scores is evaluated separately under the respective weightage. As a result, each factor is given a unique value based on the calculations from the credit scoring models.

Depending on the model used by the credit bureaus, some elements in the model will be relatively more important than others and, hence, will have a more significant influence on the credit score. For example, payment history will account for 35% for the FICO scoring model and 40% for the Vantage scoring model, and 10% will be given to the credit mix for both models.

So it is apparent that different credit scoring models will bring different results for each model category.

Let us look into factors that can result in a good credit score for a person.

How Can a Person Improve the Credit Scores?

In this section, we will study those factors that a person should adhere to if they wish to bring an improvement to their credit scores. They include the following:

Make at Least Minimum Payment and Make All Debt Payments Before the Due Date

Financial experts advise that people should at least make some payment on their dues rather than paying no payments. Not paying the full payment will cause more severe damage to the credit score than those who pay something. Consider the phrase “something is better than nothing”, which argues that doing something is beneficial rather than not doing it. The exact phrase applies to matters like debt payments.

Moreover, all payments must be made promptly to prevent damage to the credit score. Missing a payment will damage the credit score as it will stay on the credit report for seven years. People seem to prolong their dues until the late payment date, and when that date arrives, they do not have the funds to pay all their dues. And some people even forget about their financial responsibilities.

Keep Your Credit Card Balances Low

The credit utilization rate should be less than 30%, representing the debt to income ratio. So all the debt should be paid back in time to prevent it from going beyond the 30% limit. A low credit utilization rate would mean that a person has relatively less debt than they have to pay to the creditors, which shows a healthy financial condition. Any unpaid debt is a liability that will decrease the credit score. People in the excellent credit score category have a credit utilization ratio in single digits, which denotes less risk.

Get Credit Accounts That the Credit Bureaus acknowledge

Having fewer credit accounts makes it easy to maintain the financial. Those credit accounts must be reported to the credit bureaus that take credit balance being paid on time. This will cause an improvement in the credit score. People can opt for installment accounts, student accounts, personal loans, and mortgages that can be easily maintained and paid off on time to avoid such inconvenience.

Only Apply for Credit When You Need It

There is a possibility that opening a new credit account may result in a hard inquiry which will show up on the credit report and cause damage to the credit score. So it is advised to apply for credit when in need of it. At times, people apply for credit and do not pay it on time, making them financially weak. Although the impact of new credit is only 10% if someone applies for new credit back to back or frequently, the impact will be significant and will cause a decrease in the credit score.

How Can a Person Harm their Credit Score?

Here, we will look into those factors that can damage the credit score. They include the following:

Bankruptcy

Increasing a credit score can take years of hard work, on-time payments, etc., but it can take a single act to decrease it by hundreds of points. These points are directly related to filing for bankruptcy which means a person does not have the financial capabilities to pay back the debt they already own. Many people utilize credit more than they can afford, declaring themselves bankrupt. As a result, a black mark is put on their credit report, negatively impacting their credit score for a year.

For ten years, the bankruptcy note will be part of the credit report and should only be used as a last resort. Financial experts say that people should avoid getting themselves in this situation as it is difficult to get out. People cannot get approval for a loan or other lines of credit after being declared bankrupt. The reason is that lenders will see this as a very risky investment with no assurance that it will be returned.

Foreclosure

If a person has missed their mortgage payments in the past, the bank or the creditor is within the rights as per the terms and conditions to take ownership of the property. The borrower will have to vacate the property and get a foreclosure mark on their credit report. This black mark will be part of the credit report for seven years. It will inflict an adverse response on the credit score during this time. It will take a lot of time and effort to remove this black, so it is advisable not to put yourself in this situation.

High Credit Utilization

Credit utilization measures the debt owed to the overall credit limit, directly impacting the credit score. If a person has used more than 30% of their lines of credit and the debt is left unpaid, it will show unhealthy financial standing. As a result, the credit bureaus may see this as a reason to depress the credit scores. A smart move is to move your credit between cards with less or no interest rate to decrease the amount owed.

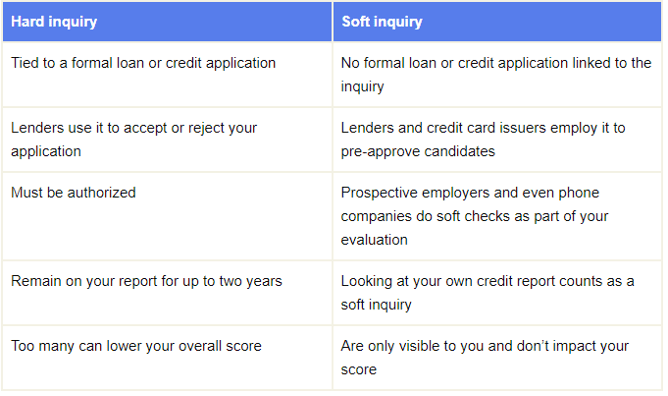

Credit Inquiries

There are two types of credit inquiries that lenders carry out to check if you are suitable for the credit. A soft pull is the first one that has no impact on the credit score as it does not appear on the credit report. A hard inquiry is the other one that does appear on the credit score and brings negative consequences to the credit score. So it is better to apply for credit that is of imminent need and does not have unpaid dues as they all accumulate to decrease the credit points.

To draw a comparison between soft pull and hard inquiry, see the following:

Let us look at the different ways to achieve a credit score.

How Can a Person Check Their Credit Scores for Free?

Before going to a lender for a loan or lines of credit, it is vital to know where you stand financially. And to get a good picture of it, a person needs to evaluate their credit score. Most people prefer to do that free of cost. People can access several websites, but they all ask for personal information, so it is better to trust the official websites.

This section will look at the trusted sources a person can use to know about their credit score, which will not charge them. They include the following:

Visit a Free Credit Scoring Website

Although numerous websites are worth visiting, financial experts advise using the website annual credit report. A person can sign up for free and put in their details to get a copy of their credit report. The website does not ask for any irrelevant information, and it is free of cost. But it is essential to read the terms and conditions before signing up as a precautionary measure. Another website that is legit and offers credit scores for free is Experian. This is one of the credit bureaus that provide free credit reports to anyone looking to check their credit score.

Check With Your Credit Card Issuer or Lender

Several credit card companies and creditors offer such a service for free, and a person can reach out to them to know about their credit scores. You would need to sign up and log in to the account you have created at the company’s website and check your credit score for free. Chase is an example of it. Prospective clients can log in to their accounts and receive monthly credit reports for free. Similarly, other credit card companies offer such a service and do not charge anything. This is their strategy to attract clients.

Visit a Nonprofit Credit Counselor

Credit counselors in the industry can take out your credit report for free if you provide them with the necessary information. National Foundation for Credit Counseling is known to help those seeking to locate someone near them who can help them with their credit report.

Frequently Asked Questions

How Often Should You Check Your Credit Score?

Financial experts advise checking the credit score every month to know where you stand financially. It is recommended to check out websites and credit card companies for a free credit report before applying for any loan or line of credit.

What Is the Credit Score Range?

Both FICO and Vantage scoring models share a similar credit score range that starts from a minimum of 300 credit scores to a maximum of 850 credit scores. Good credit is considered that is north of a 670 credit score.

How Is Credit Score Calculated?

Credit score depends on five factors which include the following

- Payment history 35%

- Debt owed 30%

- Length of credit history 15%

- Credit Mix 10%

- New Credit 10%

The credit score is calculated separately for each category and given a specific value.

How Long Does It Take To Get a Good Credit Score?

Everyone has different financial conditions, so getting a good credit score might take only months, while others at a beginner level might take a few years.

How Do I Find Out What My Credit Scores Are?

Anyone can check their credit scores free from the major credit bureaus, including Experian, TransUnion, and Equifax. A person can also ask their credit card companies to issue their credit score through a credit report.

Conclusion

This article will help you understand your credit score and how to improve it and calculate the credit report for free. You will also understand what factors affect the credit score and how to eliminate them. Conclusion: there are certain long-term factors, and we talked about how to avoid them for a good credit score.

A credit score is a number that is important for you to get a loan or line of credit. It is the first thing that creditors look at. People have different financial conditions, so their credit scores will also differ. The credit score depicts a person’s financial standing and how they treat their finances. A credit score has different factors that impact it. They include payment history, credit mix, new credit, amounts owed, etc. Adhering to all these factors can improve your credit score, and those who follow it have excellent credit scores that result in reward credit cards, higher credit limits, low credit scores, etc.

Credit scores are divided into two categories: good or bad credit scores. Good credit score borrowers enjoy favorable terms and conditions. In contrast, bad credit score borrowers are not approved for credit or loans or get approval with unfavorable conditions like short repayment periods and higher interests.