Bad credit is the leading factor that prevents people from getting loans, mortgages, etc., at favorable terms and conditions. Bad credit means bad news for a person who is not paying their dues on time. Bad credit would hinder achieving financial milestones like paying off credit card debt.

When a person applies for a loan such as a car loan or home loan, the creditor will look at their credit report. The credit report will show a black and white image of the individual’s financials and whether they are in an excellent position to qualify for a loan. The creditors’ primary concern is an individual’s credit score. It is a three-digit number that denotes the capability of the person to pay off the debt.

Certain factors are linked to the credit score, including payment history and debt, which speak about the individual’s record of paying back loan payments.

Bad credit is when the individual is having lower than average credit score. The average score is fixed as per different credit scoring models. These scores are found through equations that have determined a specific range to be bad, fair, good, and excellent as per the scoring model.

The article will look at the basics of a poor credit score. We will discuss the two scoring models used by creditors and a poor credit score as per these models. The article will list down the causes that result in bad credit scores. We will study the factors that are having a direct impact on credit score and their repercussions. The article will discuss the ways to improve a bad credit score.

Let’s take a look at the basics of bad credit score to understand it better.

Fundamentals of a Bad Credit Score

Bad credit would mean that the person has a history where they do not pay their dues promptly. Moreover, there may be cases where the person defaults on loan payments, resulting in the lender reporting this to the credit agencies. These credit agencies keep track of everything that any person does financially.

Three major credit bureaus are keeping track of individuals through an active file. That active file will have detailed information on when a person borrowed money or applied for a loan, mortgage, or other credit. All the credit transactions and payments carried out are part of the active file.

Credit transactions and similar events could mean several things, which will include the following

- Loan application at any bank, credit union, or financial institution

- The result of the loan applications, whether they were granted or rejected

- Credit card applications at traditional banks or financial institutions

- The outcome of the credit card application, be it approval or rejection

- Credit card loans from lenders and creditors

- Foreclosures

All of the above items are part of the credit report where information on the creditor, lender, and the decision is written down to record the individual’s financial history. The credit report is accessible to any lender who wishes to know about the borrower as part of due diligence and ensures that their investment will be returned with interest. The credit report stands as the primary document determining if the person is good for the credit.

The credit score is denoted as the level of risk that the creditor would be taking by approving the credit loan for any borrower. The lower the credit score, the greater is the risk. And higher the risk, the higher the interest rate and other unfavorable terms and conditions linked to the credit.

So any person that has bad credit would also be known as the least creditworthy to pay back the loan without any default payments. A bad credit score would mean that any creditor would think twice before granting you the loan or the credit.

There have been occasions when someone with bad credit was approved for a credit card, a mortgage, or personal loans but with specific conditions. These specific conditions entailed high-interest rates on credit. Moreover, the credit card limit was short, and the repayment period was fixed, which meant that payments had to be made on a set time and date, and all dues had to be cleared.

Let us look at bad credit scores from two credit scoring models.

What is a Bad or Poor FICO Score?

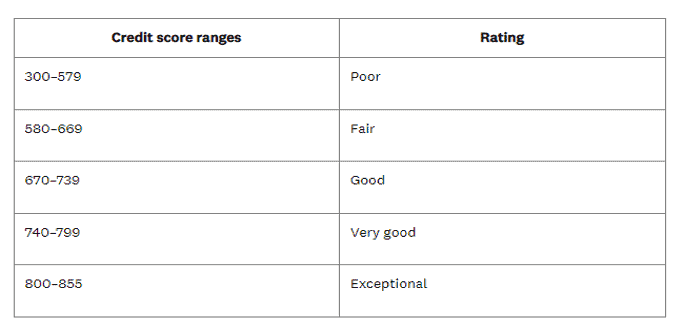

FICO scoring model is most often used as a scale to measure the creditworthiness of individuals seeking credit in some form. On the FICO scale, the credit score range is from a minimum of 300 to a maximum of 850. The higher the credit score is, the greater is the probability that a person will pay back the loan borrowed. An individual’s credit report takes out essential information regarding the financial account and payment history to evaluate the credit score.

See the table below that displays FICO scores and the specific description for each category.

As the table displays, a bad credit score is when a person falls below the 670 credit score mark because the average score per FICO is between 670-739. Specifically, if any person has a score between 580-669, that is considered fair, but a score below this range, particularly between 300-579 is considered poor.

A fair credit score person is also known as a subprime borrower. However, poor credit scores have to pay a fee or deposit as assurance that they will pay back the credit with interest. Generally, such borrowers are prone to high-interest rates on their credit.

Alternatively, those borrowers that fall in the ‘exceptional’ fico score credit rating will be given priority for the best interest rates and other favorable terms. Furthermore, borrowers with a ‘very good’ fico score credit rating are considered next to ‘exceptional’ borrowers and are most likely to receive the credit with competitive rates. Those with a ‘good’ fico score credit rating may be approved but not at competitive rates.

What Is a Bad or Poor Vantage Score?

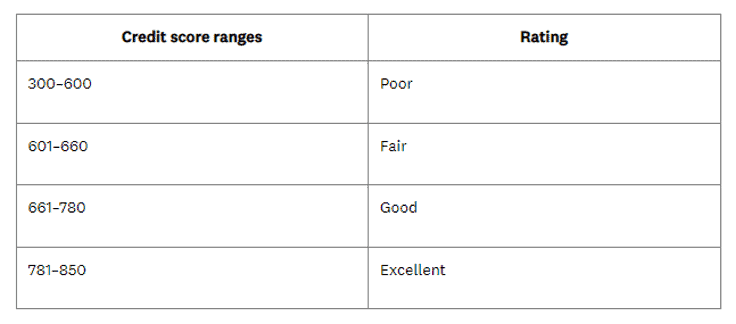

The Vantage scoring model is another model that lenders use to evaluate the creditworthiness of the borrowers. The major credit bureaus tasked to create credit reports and keep a check on individuals’ finance and account activities also consider using this model. But the description of each range varies from that to the FICO scale. A greater vantage score ensures that all credit and related queries get instant approval.

Check the table below that displays Vantage scores and the specific description for each category.

According to the table, a vantage score below 661 is considered not good, decreasing the chance of getting the credit with favorable terms. A vantage score that falls in the range of 601-660 will be treated as fair, and that in the 300-600 range will be considered very bad. The lower the credit score, the higher is the probability of getting a rejection on credit.

Borrowers with ‘excellent’ vantage score credit rating will receive the best and most favorable interest rates and favorable terms and conditions on credit. Moreover, those will a ‘good’ vantage score credit rating will receive competitive rates that suit their credit score, and they would most likely get approved for the credit.

Alternatively, those with a ‘fair’ vantage score credit rating will be assessed based on their credit report, and the interest rate will differ for each borrower. Hence, the interest rates will not be competitive; the probability of being approved will be subjected to their financial history.

Similarly, there will be borrowers that fall in the ‘poor’ vantage score credit rating, which means they will fall in these two extremes:

- Either the borrower’s application will be rejected due to poor credit performance as per their credit report, or

- Some creditors may grant their application across the approval phase but with higher interest rates and unfavorable terms, such as a greater down payment.

Let us look at the mainstream causes of bad credit that people often fall into.

What are Bad Credit Causes?

There can be several reasons that the lender can bring up to cause a rejection in the credit. Bad credits appear because the person could not meet their financial liabilities on time, which was noted in their credit report. These reasons prove that the individual will not pay back or default on payments. So the lender is entitled to report it to the credit bureaus, which then becomes part of the person’s credit history that future creditors can see.

Let us look at the mainstream causes of bad credit.

Late Payments

An individual’s payment history accounts for all the transactions and payments that happened in the past and is kept at a record, accounting for about 35%. Suppose a person has delayed in making the payments happen. In that case, the creditor will report this slacking behavior along with the credit’s amount and terms and conditions to the credit agencies who will record it.

This information becomes part of the credit report for years to come, which means that any prospective or future creditors can look at it while assessing the person’s financial situation. Having a bad record on the credit report is not a good sign if you are looking for credit. Such a record will harm the person’s credit score for the years to come. As a result, the individual will fall into poor credit where most applications are denied.

Collection Accounts

There have been cases where the lenders cannot get their funds plus interest payment back from the borrowers due to default or late payments. In such cases, these creditors take the help of third parties to initiate the collection process to ensure the borrowers pay their dues. These third parties are known as debt collection agencies. Most lenders sell the debt the borrowers owe to these agencies to make the borrowers pay the payment before charging their accounts.

After such accounts are sold to the agencies, all the information owned by the creditor is the ownership of a debt collection agency. And this activity is included in the credit report so that the borrower is aware of the latest development. The borrowers choose to pay their dues on time if they wish to remove their bad records. Furthermore, the prospective borrowers will not approve of a loan or credit of an individual with a bad reputation for collection. Having a poor collection means that the creditors were not paid back in full promptly.

Bankruptcy Filing

There have been numerous cases where people have not fulfilled the terms and conditions of their credit righteously, and as such, they have defaulted on payments. When such default payments continue to happen, and people cannot pay off their dues, they will have no option other than to file for bankruptcy. This would also mean that now these people will receive legal protection to help them get out of this financial trouble.

While bankruptcy protects the borrowers legally, it has a huge impact on the credit score, which would be substantially low in the post-bankruptcy period. And it will take several years to repair that damage. Bankruptcy filing is an act that will be recorded in the credit report, which means that any future lender can see to it and would know how risky it would be to grant such an individuals loan or credit. It is believed that the bankruptcy record stays part of the credit report for about seven years, inflicting damage to the credit score.

Charge-offs

If an account has remained inactive for far too long, it may be treated as dormant and will be charged off. A charge off account would mean that the lender is not pursuing the account holder to pay their dues which would leave a black mark on the credit report damaging it even further. A charge-off account is considered dormant and is no longer operational, which means this account will not see any further transactions from the borrower’s end.

As a result of the charge-off account, the credit report will show a charge-off credit amount in the credit report. Having a credit balance in the credit report is never good for any lender assessing a prospective borrower’s credit report. The charge-off balance will continue to damage the credit score until it is fully paid and other dues. The charge off account activity is reported to the credit bureaus, making it part of the credit report for the next seven years.

Defaulting on Loans

The defaulted loans are treated similarly to the charge-off account, adversely affecting the credit score. Late payments mean that a person has not been able to pay off their dues on time, and if that period exceeds a month, it is considered a default. So a default payment would involve a missed payment for any month.

The default payment information will be forwarded to the major credit bureaus to make it become part of that individual’s credit report. Doing so will cause a decrease in the individual’s credit score, which would make future loans hard to approve. Hence, prospective creditors will access the credit report and view the borrower as a risky investment that would cause them trouble in the future.

Let us look at the factors that directly impact the credit score.

What Affects Your Credit Score?

In the previous section, we discussed the mainstream reasons that cause damage to the credit score of an individual. In this section, we will discuss some other factors that inflict the credit score in one way or another. These factors directly impact a person’s creditworthiness, and hence it is important to know about them. They include the following:

Credit Utilization Ratio

The credit utilization rate is measured in percentage that shows how much of the available credit a person is using at any given time. It is advised to be less than 30% if a person is looking to ask for a loan or credit in most cases. The credit utilization ratio is evaluated on the debt a person is into, which includes the credit they have utilized relative to the total credit they are allowed to use. The higher the credit utilization ratio, the lower is the credit score.

Financial experts advise that borrowers looking to get a good interest rate, credit, and terms for the credit should keep the credit utilization ratio below 6%.

Length of Credit History

This factor accounts for 15% of the credit score, which is a good enough number to impact the credit score and cause a decrease. So it is advised to cater towards it with care. Length of the credit history accounts for the overall time the account has been opened in the credit report. The greater the number, the better it is for the credit score.

That is why the older accounts are more easily prone to be given credit or loans because of their credit history. With new accounts, the issue is that they don’t have a credit history, so their credit score is low.

New Credit

This factor accounts for 10% of the overall credit score, so it is advised to cater to the credit with care and only buy the necessary items with credit or loan. The credit report will include a separate category for new credit, which tells if the person has applied for any new form of credit. People are discouraged from applying for new credit in a short period as that will adversely impact their new credit category. So, the lenders might see it as financial trouble on behalf of the borrower. Hence, they might not agree on the credit.

Credit Mix

Credit mix accounts for 10% of the overall credit score and should be treated with importance. As the name suggests, a good credit mix will include credit of all sorts like credit cards, loans, mortgages, etc., which will show that a person can manage all types of credit accounts. This would mean that they are good at making the payments on time, positively impacting their credit score.

We will now look at how bad credit can adversely affect an individual.

How a Poor Credit Score Can Affect You

We have discussed the factors that can directly impact the credit score. We also talked about other factors that inflict the credit score adversely. This section will see the negative consequences of those factors on a person who has a bad or poor credit score.

There are several ways in which bad credit can impact you, which include the following:

Higher Interest Rates

Individuals with a bad credit score are often seen as highly risky investments. So the creditors would choose not to approve your credit application, but there will be certain limitations in the case it’s the opposite. One of the mainstream conditions is imposing a high-interest rate on credit, which would mean greater interest payment.

The high-interest rate is due to the high risk a creditor is taking by granting you the loan, which could lead to default payment, and the creditor will have to suffer loss for it. So no matter what kind of credit you are asking for, if the credit score is in the bad or poor category, a person would need to pay higher interest.

Trouble Getting a Mortgage

Mortgages on cars, houses, etc., are considered very large loans, which are different from other kinds of credit like a credit card. So these loans demand greater insurance that the funds will be paid back to the creditor along with the interest payment on the agreed APR set in the terms and conditions. Such loans demand that the borrower’s financial situation speak for itself and that lenders are assured that the investment will not default at any given time.

Several creditors in the market have a different mindset on how they work. While some lenders would immediately reject the application based on poor credit score, others might accept it with the condition of high-interest payment.

Risk of Being Denied Credit

There is always a risk of applying for new credit as a person would not know whether it will be approved or rejected. So if a person has been managing their financials poorly, which would mean that they are not paying their dues on time, and have a lot of debt on hand, then the application might not be approved. As a result, this rejection would be written in the individual’s credit report, further damaging their credit score.

Risk of Being Turned Down For a Job

There have been occasions where employers have rejected candidates based on their financial situation. They believe that how a person manages their finances is similar to how they would manage their work. So if anyone wants to know how a person would be at any job, they should look at how they cope with their financial situation.

On several occasions, employers have asked for the credit report of a candidate who is seeking to work for a given company. The credit report will show a clear picture of how a person stands financially. If they notice anything irregular about your credit report, such as bankruptcy filing, charge-off balance, etc., they might not be in favor of giving the person that job. Many financial jobs like financial analysts rely on individual capabilities to manage their finances.

Difficulty Obtaining Loans

Loans can be segregated into categories. One type of loan is a personal loan. These loans can be asked for an auto loan, house or apartment loan, etc. Another type of loan is a business loan. They can include a credit amount to pay off immediate debt like a mortgage. When a person has poor credit, it won’t be easy to approve either of the two types of loans because the creditors do not believe that you will pay them back with interest.

When a person asks for a business loan and sees their credit history having black marks, which shows the inability to pay the dues back, the application for loan approval will be rejected. Similarly, if someone asks for a loan for an apartment, it comes at a greater risk to be granted. The lenders do not want to lose their money by investing in someone that will default or declare bankruptcy.

The same is the case with a rental application loan, as it is very difficult to be approved since the owner will do a background check to know more about you and your financial situation. Hence, they will find your credit report having black marks indicating that you cannot pay back the payment. So any owner would not have you as their tenant because they can’t deal with the risk and trouble.

There are similar cases in getting products like an internet connection or a cell phone on loan. The companies that deal with such products and services apply for your credit report, and if they see that you are not good to pay them back, they will not approve the loan.

Let us now look at the factors that can help a person improve their bad credit score.

How to Improve a Bad Credit Score

In the previous section, we look at several repercussions of bad credit. This section will discuss how to resolve those issues and get rid of them efficiently. The credit report can be made better by working on those factors that are causing a hindrance in getting a good credit score. Although every person would have different factors linking to a low credit score, the reasons will typically be from those stated below. They include the following:

Check Your Credit Score for Free

The first step any individual should carry out as part of their due diligence is to check their credit report for free. The credit report will show them a true picture of their standing and whether the score is good enough to apply for credit. Several websites will check your credit report for free. One of the most famous ones that many creditors use is Annual Credit Report.

The credit report will show the individual all the factors that are causing damage to their credit score, and they can work on improving or eliminating those factors. Any unpaid dues should be cleared off first, and all credit balances should be written off as soon as possible.

The credit report is prone to errors that inflict damage on the credit report, and as such, they should be reported to the credit bureaus for rectification. There have been occasions when wrong personal information was included as someone else’s, which is a fraud and should be reported. As a result, a dispute should be reported to the agencies which do not affect credit score.

Pay Your Bills on Time

Payment history contributes to the largest factors that affect the credit score, which is 35%, and as such, it should be treated with immediate priority. This means that the credit score is highly dependent on how often a person pays their bills on time. Most importantly, they would need to cater towards their credit like loan payments or mortgage and debt payments which contribute to a large proportion of the credit score.

Suppose a person has a lot of credit payments to carry out in a month. In that case, it is better to pay early to avoid any inconvenience relative to pushing it further to the due date and resulting in being unable to pay on time. People early put out a good image to the creditors as they develop trust in you and would help you out in the event when a certain unexpected thing happens that requires an influx of cash like a medical emergency.

Bills can include utility bills, loans, credit card bills, and any other line of credit to be paid by the borrower. Banks and creditors have made it easy for people to pay bills by using apps to pay bills online without doing much hassle.

Avoid New Hard Inquiries

If a person wants to improve their credit score, they should refrain from applying for new credit, which would result in a hard inquiry. Whenever a creditor carries out a hard pull on your account, it directly impacts your credit score, as written down in the credit report by the credit bureaus. A hard inquiry is made because lenders think that a person is at risk of paying back their dues on time, so they carry it out to ensure their investment is safe.

It is advised to not apply for new credit while improving your credit score and to carry out due diligence about the creditors, and if they are good with making a soft inquiry, then that’s the safest option. A soft inquiry has no impact on the credit score, so it is a reasonable option, but it depends on the creditor.

Get Credit Building Help

If a person is looking to apply for a loan but has a poor credit score, it is advised to get help from a co-signer. A co-signer is a person that has a good crediting rating relative to yours and provides a guarantee and assurance that the person will not default on payments and all dues will be paid timely. The co-signer has a decent income which is one of the factors that can increase the probability of loan approval. The co-signer can pay back the loan to speed up the process with the borrower.

Another way to build the credit score positively is to become an authorized user on a credit card where the borrower takes the help of a friend or family member. The person can add you as part of immediate or close family, improving the odds of getting a loan or credit card. Ensuring that the person has a good credit history, stable income, and no debt or credit balance is important. These factors ensure that he is good at making the payments.

Get a Secured Credit Card

A secured credit card comes with the condition that the person would need to pay a deposit as security which would be kept as collateral. The amount you deposit will serve as the credit limit, and the good thing about secured cards is that when you pay the dues, the creditor reports it to the major credit bureaus. Hence, that would help you improve your credit score.

Apply for a Short Term Loan

People can also apply for a short-term loan to be paid back within a year. Short-term loans are unsecured loans, so they do not need any security deposit to be paid as collateral. Paying back short-term loans will have a positive impact on the credit score. There are different short-term loans a person can apply for as per their needs and preference.

Conclusion

So now you know exactly “what is bad credit?“. Yes, bad credit is bad news for anyone who wishes to apply for a loan or line of credit. The creditors do not acknowledge people that have bad credit as they believe it is too risky for them to invest it. Bad credit is the product of unpaid dues, late payments, default payments, etc. These factors inflict damage on the credit score.

A bad credit score can be improved by catering to its causes. In the article, we have discussed several reasons that cause an individual to have bad credit, and so there are ways to tackle it. The article consists of several ways to improve the credit score for anyone who wishes to apply for a new credit card or loan, be it for a house or car. Having a positive or good credit score is never an issue, but having bad credit can have serious consequences if left untreated. So it is advised by financial experts to eliminate the causes effectively and efficiently.