Several companies provide life insurance quotes which consist of rates, term lengths, and the coverage amount. Prospective life insurance holders have to choose the best company they see would fit their requirements perfectly, such as their needs and wants. Some people also consider the cost they would have to bear to sign up for particular life insurance. People tend to choose life insurance policies based on their financial condition.

Life insurance quotes will differ for each person, even in the same family, as the company will consider their sex, age, health conditions, and other crucial factors. People typically go after cheap life insurance quotes because they look tempting and cost-effective. However, financial experts advise choosing that insurance company and that specific life insurance quote that can cover you or your family in times of hardships. Worst scenarios can come on anyone, so it is better to be fully insured to be safe.

To select the best life insurance company, one needs to know about life insurance and its related branches. For instance, an individual looking for life insurance should know how to choose the top life insurance quotes by shortlisting the best one that fits their taste and preference. Since life insurance quotes estimate the insurance premium a person would have to pay if they were to select this one, it is imperative to have the basic knowledge.

People can get their hands on life insurance quotes through the website of the insurance providers, insurance agents, or insurance intermediaries that work with several insurance companies. Some companies make it convenient for prospective policyholders to know about the insurance quotes through their online platforms.

It is crucial to know that the same insurance policy will differ for each insurance provider. While some insurance providers will charge less, others will cost you more because of their reputation and insurance plan. Price is an essential factor in determining the insurance policy, but it should not remain the only factor that any person should consider.

Insurance companies have their ways of valuing and evaluating risk. This means they would see your financial background and determine if you will be able to pay for the insurance policy without any delays. The higher the risk, the less is the probability that a person would get favorable insurance quotes. Some factors come into play when looking at a person’s financial background, such as their assets, liabilities, liquidity available, property, and other benefits.

This guide will cover some basics of life insurance by focusing more on life insurance quotes. We will cover how to get a life insurance quote that factors into applying for a life insurance policy. So the guide will discuss the steps to use for a life insurance quote and hence, the life insurance. We will also discuss factors that every individual should consider before agreeing on a life insurance policy. The article will discuss the factors that come into play in determining the life insurance quotes that the person would be assigned. A FAQs section will be added to answer general questions about life insurance quotes.

Why Do I Need Life Insurance?

The main reason people opt for life insurance is to ensure the safety of their families regarding their financial needs in the future. People are optimistic about their lives, so they wish to safeguard their families from any financial trouble if they die. Individuals want to make sure that their families will receive a tax-free payout that will help them fulfill their financial needs. Although money is not essential, it can help the beneficiaries if the breadwinner is deceased.

Through life insurance, the family, beneficiaries can do the following:

- The family can pay for the expenses that will be incurred after your death, such as funeral costs and burial expenses

- The life insurance amount can be used as an alternative to paying for the bills and necessary expenses that will include utility bills, college tuition, groceries, etc.

- The beneficiaries can use some part of the amount to pay for any loan payments like car and house mortgages which should be paid on time; otherwise, the borrower will have to pay interest

- If the family consists of young children, then the amount can go into childcare, like hiring a nanny or paying for the needs of a child

- People can use the life insurance as savings to be used as retirement funds

- Some people leave money back in the form of inheritance that the children can use to pay off fees for their education purpose, etc

- Several people wish to donate money, but they are unable to carry out this noble act and thus buy life insurance; the funds would go to a charitable organization as a noble cause

People have different views on how they perceive life insurance. While some wish to use it for themselves as retirement money, others value their family’s financial situation and buy it.

What Should a Person Know Before Getting Life Insurance Quotes?

Several misconceptions about life insurance cause people to make decisions that hurt their financial situation. The reason is that such people do not carry out the due diligence they need to before agreeing on life insurance with a designated insurance provider. Financial experts advise people to know about companies’ offerings and their compatibility with their preferences before deciding.

A prospective policyholder should be aware of the following

Life Insurance Is More Affordable Than You Think

One misconception people have about life insurance is that it is expensive to purchase and pay for over the long run. However, that is not the case as people who say that do not have the appropriate knowledge to support it. For instance, if a person in their 30s wishes to purchase term life insurance with 20 years of coverage with a death penalty of a quarter million, they would need to pay 165 USD a year. This means they have to pay about 13 USD a month which any person can pay. The stated amount is the average amount for people in their 30s. Check out this study to know more!

Buy Life Insurance When You Are Younger

Financial experts advise buying life insurance at a younger age because it is more affordable. It caters to several factors that turn out to be favorable for prospective policyholders. The insurance provider would value your age and health and factor in signing a quote (also known as a premium) that the person would have to pay. People who tend to wait till they are old enough are prone to more health risks and, as such, will get unfavorable quotes.

You Might Not Need a Medical Exam

Although it is mandatory to get a medical check-up to opt for life insurance, specific policies are designed not to require a medical exam. Although the quantity of policies in the market that ask for a medical exam is more, several good policies do not need you to undergo a medical exam. Several insurance providers are available in the industry that offers 30-year coverage on life insurance without a medical exam.

With varying terms and coverage amounts, you can be assured that there are options in the industry. Some insurance providers also provide an offer where a person can convert their existing policy to permanent life insurance.

The Application Process Can Be Fast and Easy

The application process takes different times depending on several factors, including the insurance provider, your overall profile, and the type of insurance you are looking to purchase. The processing time for candidates that have passed the screening process is relatively less than for those individuals whose profile needs time to evaluate. Prospective policyholders in good health and young age can apply on the insurance provider’s online platform and get approval within a few minutes.

A person’s profile has to do a lot with the processing time. If your profile is good, you will not need a medical exam and can get approved for life insurance promptly.

Compare Life Insurance Quotes from Several Insurers

If you are new and do not have relevant information for life insurance, it is better to take help from a financial expert or insurance broker. Depending on your financial conditions, they know which companies will be most suitable for you. Since prices vary for each insurance provider and the insurance policies offered in the market, it is best to find one that matches your wants and needs.

How to Get a Life Insurance Quote?

In the previous section, we looked at the mandatory factors for a person before they opt for particular life insurance. These factors cover the due diligence part of the insurance policies at the prospective policyholder’s end. Here, we will look at the different steps a person should follow to secure a life insurance quote. Let’s get started!

People often do not take the necessary steps to get a life insurance quote, leaving them underinsured. Underinsured is a term used to describe a person whose life insurance will not cover their family’s financial responsibilities.

Financial experts have laid out the following steps to provide you with a life insurance plan and coverage suitable to your needs. They include the following

Calculate Your Life Insurance Needs

The first step in understanding how much life insurance a prospective policyholder would need is to evaluate their financial obligations and the number of financial resources available at their disposal. People who approach life insurance brokers and agents know that their financial resources are inadequate to cover their family’s financial obligations.

The primary purpose of life insurance is to provide enough life insurance coverage that the person would not have been able to manage on their own. Some people have a greater demand that requires a relatively more significant life insurance coverage as they wish to leave a legacy behind in a charitable organization.

Certain financial obligations are common for all prospective policyholders. They include:

Funeral and Burial Expenses

According to National Funeral Directors Association, the average funeral cost in the United costs for a working-class person is $7640, which caters to funeral proceedings and burial expenses.

Income Replacement

Life insurance can serve multiple purposes as an alternative to the income earned by the breadwinner(policyholder). It can be used against the person’s income to put food on the table and provide the children with the necessary education. Hence, people should evaluate how much of their income would be replaced with the same amount that would count for life insurance. At this point, you are required to cater to the coverage term. Some people evaluate till their children’s graduation.

Debts You Owe

The debts mainly consist of the mortgage payment that is still due, which the person would need to pay, and in their absence, their family would have to. The situation may differ on the mortgage value and the type of mortgage the person has signed up for. Moreover, if the person has other kinds of debts, they should be accounted for all the future payments still due.

Child Care

Some people have toddlers or young children whose responsibility and catering to their financial needs is the sole responsibility of the parents. Hence, the policyholder would need to see the amount it would cost to raise the children, the kind of luxuries they will be prone to, and its expense.

If both the parents are career-oriented, they would need a nanny that would take care of their children while they are away, so this would cost them, and so the person needs to evaluate the average hourly rate and the tenure for child support.

College Tuition

Every parent’s dream is to see their children graduate, so it is vital to fulfilling that dream; the policyholder plans ahead. You would need to see the average tuition cost and multiply that by the number of children to evaluate the funds you would need in the future.

Evaluate Life Insurance Companies

When a person purchases a life insurance policy, they get involved in a long-term commitment with the insurance providers. As a result, any prospective policyholder must be in business with a designated insurance provider that has an excellent reputation in the market. This reputation would stand as the fundamentals of establishing an excellent long-term relationship with the insurance company.

Moreover, a person would need to ensure that the company should fulfill your needs at a fair price apart from reputation. Hence, a person should consider the insurance quotes that each insurance provider submits to the prospective policyholder detailing insurance premium coverage amount information.

Other essential factors to consider will include the terms and conditions the insurer is offering, such as the possibility of changing a term life insurance policy to permanent life insurance. Different life insurance companies have varying rules and regulations on their insurance policies. Hence, it is ideal for comparing them based on specific factors. The factors may include how reliable their policy illustrations are, the company’s low policy expenses, and the top financial strength of the insurance providers that set them different from other companies.

Gather Your Information

Since you are looking to purchase a life insurance policy, you must have relevant documents that the insurance provider will ask for. People need to provide some basic information about themselves to avail life insurance quotes. The data can get specific from one insurance provider to another, but some general information that all insurance companies ask for includes:

- The weight and height of the person looking to purchase the insurance policy

- The medical history of the prospective policyholder, including ongoing or past health conditions

- The medical history of the family, such as any underlying medical conditions in the family-like heart disease, diabetes among parents and siblings

- The medications the prospective policyholder is currently under or was taking in the past

Such medical records are essential to qualify for a lie insurance policy. If the person does not provide the correct information, their application will be rejected. In some cases, people have been blacklisted, which means they can not apply to the company again.

Compare Life Insurance Quotes

Financial experts advise finding a reasonable price on a life insurance policy that will fit your needs by comparing the life insurance quotes from different insurance providers. In some instances, people can also qualify for free insurance quotes, which may depend on one company to another.

Free quotes are available online as different companies upload them on their websites for the users’ convenience and make the process efficient yet effective. The best way to draw a comparison would be to visit various insurance companies’ websites and check out the insurance quotes. There are designated insurance brokers with a website that lists updated insurance quotes from the companies, but you would need to pay them to avail of their services.

Free quotes are available when a person calls the insurance company or visits their office. With this process, you would need to get the help of an independent insurance agent who has connections with various insurance providers and can get you linked with different companies. In this way, you would be able to compare the quotes and see which ones would fit your needs perfectly.

What Factors Are Used in Life Insurance Quotes?

In the previous section, we discussed how to get a life insurance quote. Here, we will consider all those factors that companies consider vital before issuing a life insurance quote to a prospective policyholder. Although factors may vary from one insurance provider to another, some are common for all insurance companies.

Although the mainstream factors remain the same, all companies consider your age, sex, and health conditions. For instance, women policyholders tend to pay less because they are healthier than an average man and so will live longer than them. Companies issue the lowest life insurance quotes to young men, which means they will get a favorable insurance rate and premium on their policy.

Several other factors that count towards life insurance quotes include the following

- The medical history of the prospective policyholder, which accounts for past and current records

- Medications that the prospective policyholder is taking now or before that were prescribed by the doctor

- The medical history of the person and their family members consist of immediate family members like parents and siblings

- The driving history of the person looking to purchase the life insurance policy, which includes any speeding tickets or convictions they have may get in the past

- Any criminal records like driving while under the influence of alcohol causing risky behaviors

- The dangerous hobbies the person is involved in like sky diving

- The occupation of the person, especially if it requires tasks that may be a danger to their lives

- The financial situation of the person, particularly if they have declared bankruptcy in the past

- Any criminal record that the person has had in the past

How to Apply for Life Insurance?

The following should be taken care of before you apply for a life insurance policy; putting together quotes, choosing an insurer that best suits your needs, and lastly, one that fits your budget. The kind of underwriting used in your case could vary based on your application process.

Full Underwriting

This form of underwriting is traditional because there are several steps to the process. You must complete an extensive questionnaire and undergo a life insurance medical exam. The full underwriting process then also calls for you to grant your insurer the permission they need to collect your data from diverse third-party sources.

This process will take approximately 60 days to complete, but it is also probable that the life insurance quote you may receive will be the minimum possible. This is to make sure that the pricing you’ve been given is accurate, and it only happens if you are deemed healthy from the information collected by your insurer.

Accelerated Underwriting

Though this process is similar to the traditional full underwriting process in many ways, it is dissimilar because a medical exam is not necessary here. This process is also quicker as it uses data modeling to evaluate the risk applicants may come with.

There is also the possibility of being able to apply online with this form of underwriting. In this case, getting approved for coverage will only take a few minutes as the insurer immediately collects the information required from third-party sources. Although these quotes can be compared to fully underwritten policies, the amounts covered here may only be $1 million.

Simplified Issue

The process of purchasing the simplified issue of life insurance can be relatively quick and easy compared to the others. In this process, the applicants will only be subjected to answering some questions related to their health and their lifestyle. The insurers will then do the rest by compiling other necessary information regarding the applicants.

The medical exam, in this scenario, is also not mandatory. This is so that the insurers can keep the process going and be able to decide whether to accept the applicants or not immediately. However, it is noteworthy that insurers keep their rates high to make up for the fact that insurers do not have much information on their applicants for simplified issue policies.

On the one hand, some insurers may make taking a medical exam mandatory for receiving life insurance. Alternatively, many insurers do not require taking a life insurance medical exam. Instead, they rely on evaluating and allowing healthy, young applicants to get no-exam life insurance by data modeling.

For insurers that require the completion of a medical exam, it is essential that the individual is taking it and does so in a serious manner because the outcome of the life insurance quote they are offered will be heavily based on it. Following are some of the finest tips that one can make use of to prepare themselves for the life insurance medical exam:

A few weeks before the exam, the following is recommended: limiting an intake of salt, drinking large quantities of water, and keeping up with a diet full of healthy, nutritious foods like fruits, vegetables, low-fat dairy products, and whole grains. It is also advisable to keep your alcohol consumption to a minimum.

A day before the exam, the following can be followed: abstaining completely from nicotine, alcohol, and red meat. It would also be beneficial to avoid antihistamines, decongestants, and over-the-counter medications. Lastly, it is always a good idea to get a good night’s sleep, but specifically, in this case, it will in improving your blood pressure.

It would be wise to steer clear of any caffeinated products and engage in any energy-consuming exercise on the exam day. Instead, what you should do is drink large amounts of water. Besides all of that, you must ensure that you take all required documentation with you: your medical information, photo ID, etc.

Top Life Insurance Companies That Provide the Best Quotes

The previous section looked at how a person can apply for life insurance. Here, we will discuss those companies that operate online and are considered best life insurance companies for online quotes. Let’s dive into it!

Bestow Life Insurance

Bestow life insurance is considered ideal for its straightforward application process. The company offers life insurance with short-term and long-term plan options, and the prospective policyholders can choose depending on their preference. The use of technology ensures that less paperwork is needed as the entire process works systematically.

The company provides life insurance policies that have terms from 10 years to 30 years, and people between 18 to 60 years can apply for it. The minimum policy coverage is 500,000 USD which can be covered with monthly payments of 16 USD each. The company provides maximum policy coverage is 1500,000 USD that the company offers to their clients.

Pros Include

- People do not need to undergo a medical exam to avail the policy

- The application can get approved in as little as 10 minutes

- Those who have green cards in the USA can also apply for the life insurance policy

Cons Include

- The maximum coverage is capped at $1.5 million and can only be reduced to 500,000 USD, but it cannot increase beyond the maximum limit

- The company is not known to provide the best competitive rates in the market relative to other options

Ethos Life Insurance

Ethos life insurance is considered the best value for money by clients who have had experience with the company. The company is recognized as amongst the early ones that started selling life insurance online to people. Ethos is also labeled as the pioneer for bringing in the technology that people can efficiently work with and get approved for a life insurance policy. The company offers life insurance policies for 10 to 30 years.

The company is also known to provide coverage on life insurance policies for as little as 20,000 USD to as big as $2 million. People between the ages of 25 to 65 can apply for a life insurance policy offered by the company. Those above 65 can apply for the whole life insurance policy. The coverage amount on this policy is substantially low, 1000 USD to a maximum of 30,000 USD, but this insurance’s approval rate is guaranteed.

Pros Include

- People do not need to undergo a medical exam to avail the policy, but there will be competition between the healthy applicants on who will get the insurance policy

- The application process can be completed in a matter of minutes

Cons Include

- The maximum coverage is capped at $2 million and can only be reduced to 500,000 USD, but it cannot increase beyond the maximum limit

Fabric Life Insurance

Fabric life insurance is considered ideal for those that do not want to undergo a medical exam. The company specializes in providing term life insurance policies to people without the need for a medical exam. The policies offered by the insurance provider are best suitable for those people between the ages of 25 to 60 years.

The premium that a policyholder will have to pay is as little as $6 per month, which can be managed easily. The coverage amount for the term life policy is between $100,000 to $5 million, catering to the needs of those who want a low coverage and those who require substantial coverage. The policies have terms between 10 years to 30 years.

Pros Include

- The premium is payable with debit and credit cards

- The company has a mobile app that can be accessed, and thus people can apply online

- People can receive a quote in a matter of minutes.

Cons Include

- The company has a reasonable acceptance rate, but the rates it charges its customers are considered unacceptable relative to some other options in the market

Haven Life Insurance

Haven life insurance is considered the best overall life insurance provider in the United States by the people who have bought policies from the company. The company is the pioneer in bringing the necessary technology to initiate issuing life insurance policies online. Haven life is known to provide quality life insurance policies at affordable prices that people can pay.

The application process might slightly take a longer time than some other options, and the reason is that they ask for some additional information that they deem necessary. The company provides competitive rates for those life insurance policies that do not need a medical exam.

The products they offer include a term life insurance policy for people under 60 years old, and the coverage amount for such policy is $3 million. People between the ages of 60 to 64 years are encouraged to apply and will be catered for based on their application. People in this age gap will have a coverage amount of $1 million.

Pros Include

- People can enjoy a term life insurance coverage of $3 million, which is a substantial amount for a family to fulfill their financial obligations

- The company also provides some other insurance products like disability insurance for those that are suffering from some disability

- Haven life offers income replacement coverage which covers the amount that the person was earning as their income from work

- The term life insurance offered by the company is considered cost-effective for those that find it challenging to pay the premium amount

Cons Include

- People applying for a coverage that is greater than $500,000 will require to undergo a medical exam

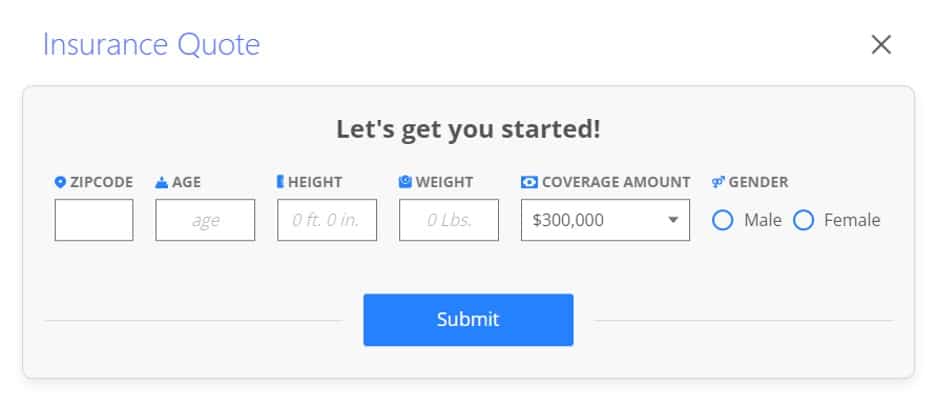

The information a person would be required to provide to the life insurance company to issue the report includes the following

- Zipcode

- Age

- Height

- Weight

- Coverage Amount

- Gender

The following image would be helpful

FAQs about Life Insurance Quotes

How Do I Get an Affordable Life Insurance Quote?

In terms of acquiring a life insurance quote based on your affordability, it would be best to do so when you are young and doing well health-wise. This is because an individual’s age and health become two of the leading factors for insurers providing you with a rate. Another reason to consider getting a quote as soon as possible is that the cost of coverage increases the longer you wait to invest in life insurance; specifically, there’s a spike every year.

At What Age Should I Buy Life Insurance?

While there is no particular age that is recommended to buy life insurance, there are certain things that you may want to consider when looking to go down this path. One would certainly be that you purchase life insurance when you feel like you need it. Though buying it earlier might mean that you can qualify for a better rate than you might get when you are relatively old, and your health isn’t what it used to be like. Certain events that may push people to purchase life insurance include getting married, investing in real estates like a house or apartment, and producing offspring.

Is Life Insurance Taxable?

While the death benefit that a beneficiary is paid usually does not account for taxable income, there are certain cases where taxes may need to be paid on life insurance. One such instance would be that investment gains on any cash value withdrawn from a permanent life insurance policy or the policy surrendered for cash will be considered taxable. However, this is not the case when all you are doing is taking a loan out of the cash value. The borrowed money here will not be taxable, given that the insurance policy does not change.

Conclusion

This article covered several topics under life insurance, specifically life insurance quotes, which are vital for any life insurance policy. Through this guide, you will be able to understand life insurance quotes and develop an understanding of them, which will enhance your knowledge. Those looking to purchase a life insurance policy will undoubtedly learn valuable information.

The guide covers different segments of life insurance policy, such as why there is a need for life insurance and what things a person should do before deciding on a life insurance policy. We covered areas of life insurance that deal with how anyone can get a life insurance quote which is necessary if they wish to find an insurer that will grant them full coverage. The article has covered all the factors that come in place which count for life insurance quotes. Knowing these factors is essential as they determine the quote you will get from the insurance provider.

Lastly, you will learn how to apply for life insurance on your own, which is essential if you do not need to avail the paid services of a life insurance agent. The steps written in the specific heading would give you all the details you need to get through the application for life insurance. So it is essential to follow the steps and keep the information and documents listed in the application process.